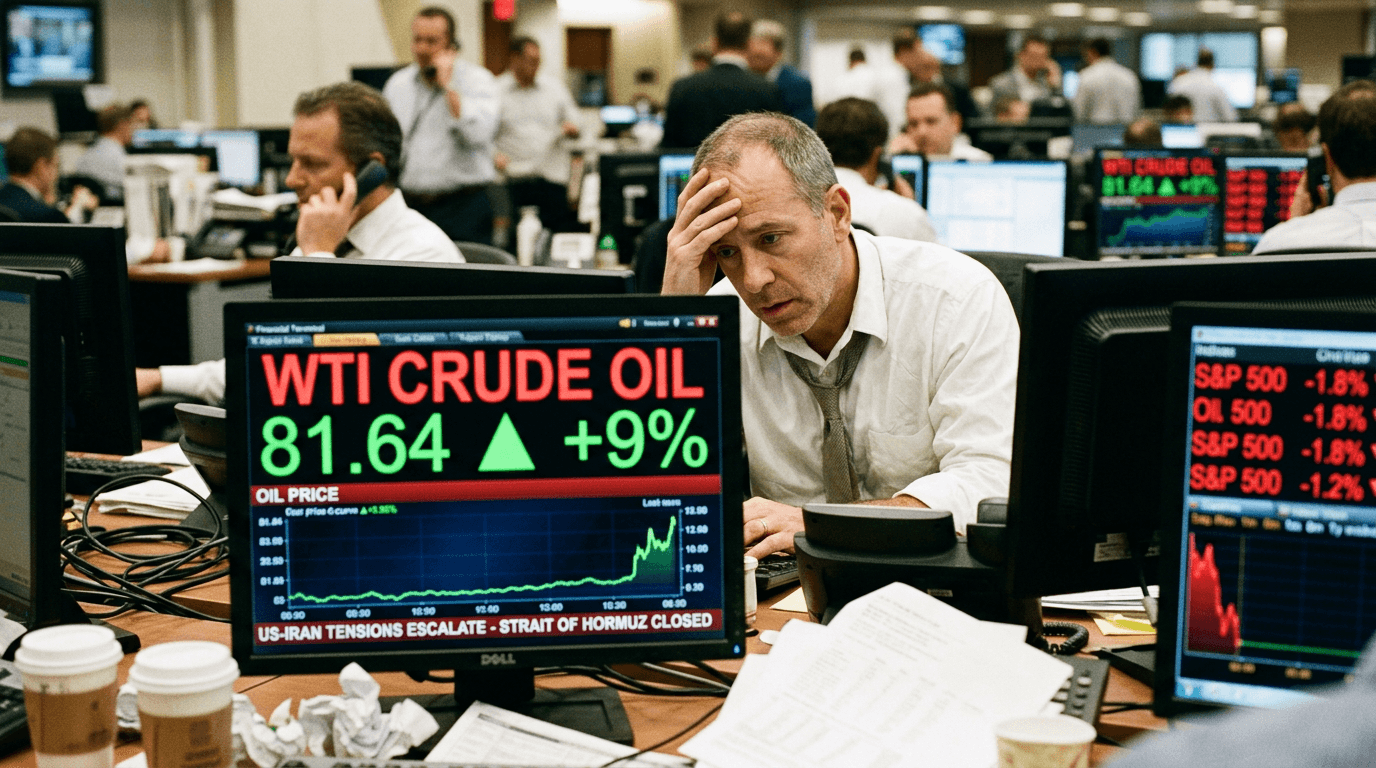

Geopolitical tensions between the United States and Iran have reached a boiling point, shaking global energy markets and unsettling investor confidence across the world. As crude oil prices climb 9% to their highest since summer 2024, both traders and investors are facing a new market paradigm. The long-held belief that Middle East disruptions can be contained has been thoroughly disproven. West Texas Intermediate crude has soared to $81.64 per barrel, while Brent crude has risen to $85.85, reflecting real supply constraints that cannot simply be reversed by shifts in sentiment or technical recoveries. For traders navigating these volatile waters, grasping the underlying dynamics is vital for managing risk and seizing opportunities.

The Conflict Reshaping Energy Markets

The escalation took a sharp turn when President Trump threatened Iran's energy infrastructure, triggering Iranian retaliation against key oil facilities and shipping routes. What began as a regional conflict has escalated into a full-blown global supply crisis, impacting one of the world's most crucial chokepoints. The closure of the Strait of Hormuz by Iran—through which nearly 20% of the global oil supply flows daily—marks an unprecedented disruption to global energy infrastructure.

The magnitude of this supply shock is unmatched in recent history. Combined military actions by Iran and the US have removed about 10 to 11 million barrels per day from the market. With global crude oil production typically around 100 million barrels daily, losing 10% of supply overnight creates a seismic event that strategic reserves struggle to mitigate. The International Energy Agency has called this the largest supply disruption in the history of the global oil market, with production from Kuwait, Iraq, Saudi Arabia, and the UAE collectively dropping by at least 10 million barrels per day since mid-March.

The physical crude oil market faces unprecedented stress, with Asian refiners paying exorbitant premiums for alternative supplies as desperation hikes acquisition costs. Norwegian Johan Sverdrup crude trading at a premium of $11.80 per barrel over Brent exemplifies buyer desperation and supply-demand imbalances that will take months to resolve.

Market Reaction And Investor Anxiety

Financial markets have responded with sharp, predictable movements, exposing deeper fears about stagflation, economic slowdown, and reduced corporate profitability. US stock indexes have declined by about 1% as investors reassess profit margins and consumer spending capacity in an increasingly inflationary climate. This classic risk-off behavior highlights genuine concerns about the complex interplay between energy prices, wage inflation, consumer demand, and economic growth.

Safe-haven assets have surged in response to equity weakness. Gold has climbed as investors seek refuge from stagflation risks, while US Treasury bonds have gained traction as portfolios shift capital from growth-focused equities to perceived safer fixed-income alternatives. This rotation underscores a fundamental shift in market sentiment: concerns about economic slowdown now outweigh the allure of higher equity valuations.

For everyday consumers, the impact is already apparent at the gas pump. National gasoline prices have risen to $3.58 per gallon, a substantial 60-cent increase in just one month. In California, prices have exceeded $5 per gallon, levels unseen since late 2023. These price hikes matter significantly as gasoline serves as the most visible, personal price index in American consumer life. When drivers fill their tanks, they confront inflation in undeniable terms that directly influence consumer sentiment, purchasing power, and overall spending behavior.

Analyzing The Downside Risks And Worst-case Scenarios

Market analysts are warning of much worse scenarios if military tensions persist and the conflict remains unresolved. If the Strait of Hormuz remains closed through June, Goldman Sachs forecasts crude oil prices could skyrocket to $200 per barrel. In such a scenario, US gasoline prices could reach considerably higher levels, and inflation could become entrenched as a persistent issue rather than a temporary cyclical challenge. These are not hypothetical exercises in pessimism but logical projections from real supply losses with no immediate replacement on global markets.

The International Energy Agency has coordinated the largest-ever emergency oil stock release of 400 million barrels to stabilize markets, yet volatility remains high and persistent. Strategic reserve releases offer tactical relief but cannot address the deep-rooted geopolitical risks and supply uncertainties fueling these price movements.

What Traders And Investors Should Monitor

Several critical factors demand close attention as this situation unfolds. First, acknowledge that this is fundamentally about real supply constraints, not speculation or market psychology. The damage to oil infrastructure and port closures are tangible, verified, and documented, not theoretical concerns. This underpins the staying power of elevated energy prices and differentiates this episode from purely sentiment-driven rallies or technical corrections.

Second, expect volatility to persist as long as the Strait of Hormuz remains closed and geopolitical uncertainty lingers. Every headline about escalation or negotiation will trigger sharp, sometimes dramatic market swings. Effective risk management and disciplined position sizing become crucial in this environment. Third, recognize that geopolitical risk premiums are now a permanent feature of market pricing. The assumption that Middle East tensions could be isolated has been unequivocally refuted.

Active monitoring of geopolitical developments combined with careful portfolio stress-testing for further escalation scenarios is vital. Energy exposure, inflation hedges, and defensive positioning all require thorough review and adjustment. The 9% surge in oil prices marks just the beginning of a major market adjustment, and only traders who understand these underlying dynamics will successfully navigate the uncertainty ahead.