A sharp global sell-off in tech and AI‑linked stocks is rippling through markets, pulling down Nasdaq and S&P 500 futures and forcing traders to reassess one of the most crowded themes of the cycle.[3][5][6] From U.S. mega-cap names to Asian chipmakers and private equity-style tech investors, the unwind is broad-based and tied to a single question: how profitable will the AI boom really be, once the infrastructure bill comes due?[3][7][8]

WHAT TRIGGERED THE TECH AND AI SELLOFF?

The immediate catalyst is growing unease about the soaring cost of building and running AI infrastructure versus the profits it is currently generating.[3][7][8] Investors are questioning whether the massive outlays on data centers, chips, networking hardware, and power can be justified by near- to medium-term earnings.[3][7]

After months of relentless inflows into AI winners and high-valuation growth names, even modest disappointments in guidance or commentary around AI spending have had outsized impact on prices.[1][3][7] Analysts have warned that expectations for AI-driven earnings upgrades have become “frothy,” leaving little margin for error when sentiment shifts.[1][7]

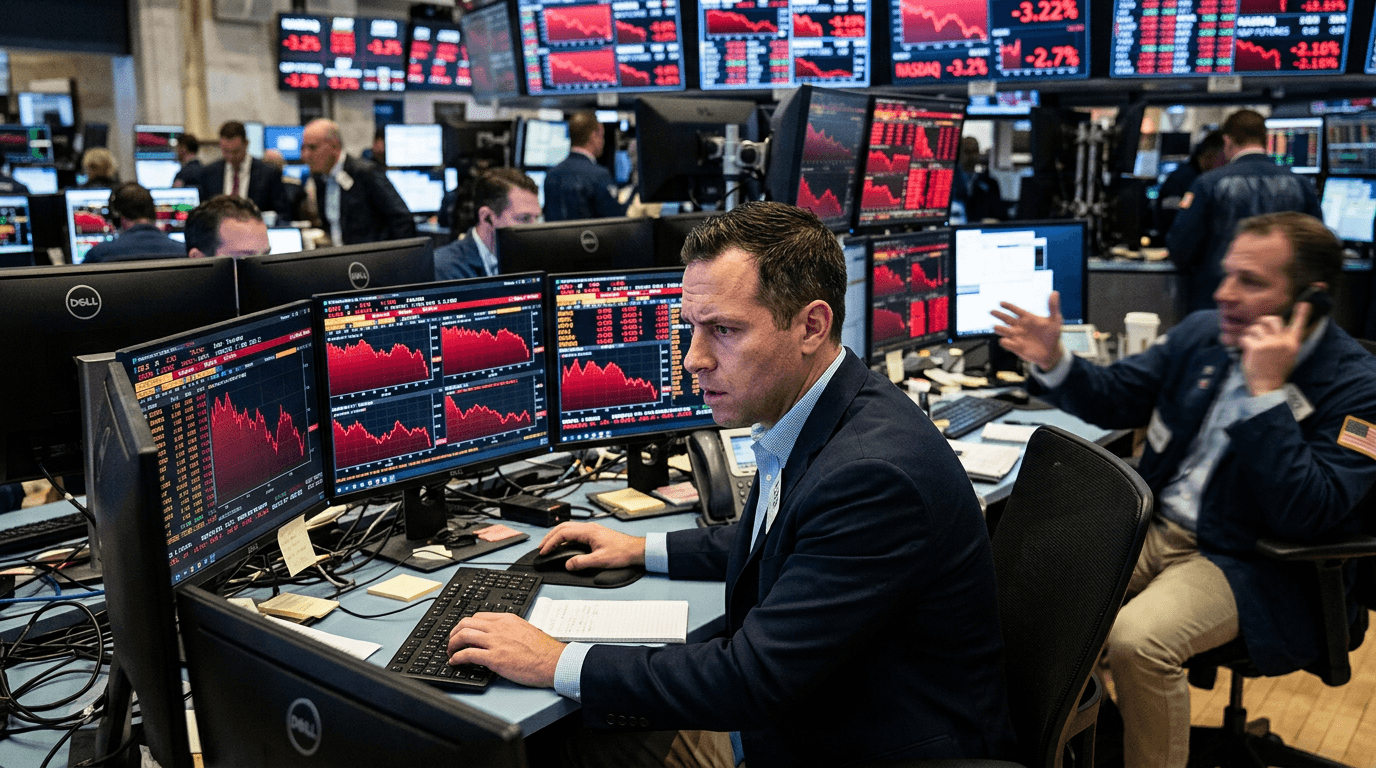

That vulnerability showed up first in U.S. trading, where major AI and semiconductor names extended prior day losses, dragging the Nasdaq Composite down more than 2% in a single session.[3][4][5] Chipmaker Micron, for example, recently fell around 13% intraday, illustrating how sensitive the space has become to any wobble in the AI thesis.[3]

How The Sell-off Went Global

What began in U.S. tech quickly became a global story. As U.S. markets slid, Asian traders woke up to a wall of red and moved to lock in profits in their own AI and semiconductor leaders.[2][4][8]

SoftBank, a high-profile investor in technology and AI-related ventures, saw its shares sink by about 12%, a move that underscored how sentiment had flipped from “buy any AI dip” to active de‑risking.[8] In South Korea, a prior episode of tech stress saw the Kospi index fall roughly 10% at one point, triggering a brief trading halt—an illustration of how concentrated tech exposure can amplify country-level volatility.[2]

Globally, AI chipmakers and hardware suppliers came under particular pressure, echoing the slide in the Philadelphia Semiconductor Index as investors rotated out of the segment.[3][4] The result has been a synchronized hit to tech-heavy benchmarks, with Nasdaq and S&P 500 futures both trading lower as the sell-off spread, pulling down broader equity indices alongside them.[3][5][6]

Warnings from major banks and strategists about potential overvaluation in AI leaders have added fuel, as investors reassess how much future growth is already priced into today’s multiples.[6][7] Some research now notes that global tech valuations have come off peak levels but still trade at a premium to the wider market, leaving them exposed when positioning is crowded.[7]

Why Nasdaq And S&p 500 Futures Are So Sensitive

Nasdaq and S&P 500 futures are reacting forcefully because a handful of large tech and AI names now account for a significant slice of index market capitalization.[3][5][6] When those leaders move together, they can dominate index performance—both on the way up and on the way down.

During the AI euphoria phase, gains in a small group of mega-cap tech firms were enough to pull the major U.S. indices to repeated record highs, despite more muted breadth beneath the surface.[2][5][6] Now the same concentration is working in reverse: a focused sell-off in AI hardware, data center, and platform names is dragging down futures, even if other sectors are relatively stable.

Futures markets are also where macro funds and systematic traders express fast views on risk sentiment. As concerns about AI profitability, valuations, and higher interest rates resurface, selling in Nasdaq and S&P 500 futures becomes a direct way to de‑risk portfolios without having to unwind every individual stock position.[3][5][6] This is part of why moves in futures can look outsized relative to the fundamental news flow on any one day.

FROM TECH ROUT TO BROADER RISK‑OFF

The AI-led decline is not just a tech story; it is morphing into a broader risk-off episode. As big tech and AI names sell off, investors are also cutting exposure in other crowded “risk-on” trades, including equity indices, FX carry positions, and crypto assets.[7][8]

High-yielding currencies funded by low-yielders, classic carry-trade structures, tend to get hit when volatility spikes and investors rush to reduce leverage.[8] The same dynamic affects speculative segments of the crypto market, where flows have increasingly tracked the broader sentiment in high-growth tech. A wobble in AI optimism therefore acts as a proxy shock for the entire high-beta complex.

For long-only equity portfolios, the shift shows up as painful drawdowns in concentrated tech allocations. For hedge funds and leveraged traders, it shows up as tighter risk limits, margin calls, and a forced reassessment of how much AI risk they truly want on the books.

Lessons For Traders And Simfi Participants

For traders — whether in live markets or on SimFi platforms — this kind of AI-led sell-off is a live case study in how narrative, positioning, and macro factors interact. Several practical takeaways stand out:

- Position size matters more than conviction. Even if you believe in the long-term AI story, oversized exposure to a single theme or sector can lead to outsized drawdowns when sentiment turns.[1][3][7]

- Valuation and expectations are part of the trade. The recent slide is not about AI disappearing; it is about how much future growth was already priced in and how quickly it can realistically be realized.[1][3][7]

- Correlations spike in stress. When AI leaders fall, related semiconductors, cloud providers, and even non-tech growth names often move together, reducing the benefits of diversification at exactly the wrong time.[3][4][6]

- Futures are a sentiment barometer. Sharp moves in Nasdaq and S&P 500 futures can signal that large players are adjusting risk, even before the cash market opens.[3][5][6]

Simulated trading environments are particularly useful in this context. They allow traders to test how their strategies would have behaved during prior AI-related drawdowns, explore hedging approaches using index futures, or experiment with factor tilts that reduce dependency on a single theme.

Navigating The Next Phase Of The Ai Trade

Looking ahead, the key question is whether this is a healthy correction within a powerful long-term trend, or the start of a more enduring de‑rating of AI-linked assets. The answer will likely hinge on three pillars:

1) Earnings and AI monetization Investors will scrutinize how quickly AI investments translate into revenue growth, margin expansion, and cash flow.[3][7][8] Companies that can clearly link AI spending to profitable use cases are more likely to regain leadership; those that cannot may face prolonged multiple compression.

2) Capex discipline and infrastructure costs Management teams that show a credible path to managing AI infrastructure costs — from chip procurement to power and cooling — without sacrificing innovation will stand out.[3][7][8] Evidence of more measured, return-focused capex could stabilize sentiment in the hardware and data center complex.

3) Macro backdrop and interest rates Higher-for-longer interest rate expectations remain a key headwind for long-duration growth assets like tech.[5][6] Any shift in central bank rhetoric, inflation data, or bond yields will feed back into valuations for AI leaders, amplifying or mitigating the current pressures.

For now, traders should assume that volatility in tech and AI-linked names will remain elevated. That creates both opportunity and risk: wide intraday ranges can be fertile ground for disciplined strategies, but they can also punish poor risk management. Using tools like simulated accounts to refine execution, stress-test portfolios, and build rule-based responses to sharp index futures moves can turn episodes like this from threats into valuable learning environments.