Market Overview: CPI Trends In Europe’s Major Economies

Greetings, traders! As we dive into a new trading week, E8 presents your vital Market Overview, providing you with crucial economic events and information that will steer your trading strategies. Stay informed about market trends and prepare for changes with our fundamental analysis.

Key Events of the Week Include:

- Inflation Rates in Japan and the Eurozone

- Reserve Bank of New Zealand (RBNZ) Interest Rate Announcement

- GDP Growth Figures for Canada, the US, and Switzerland

- Consumer Confidence Levels in the Eurozone and Japan

- Manufacturing PMI Reports from China and the US

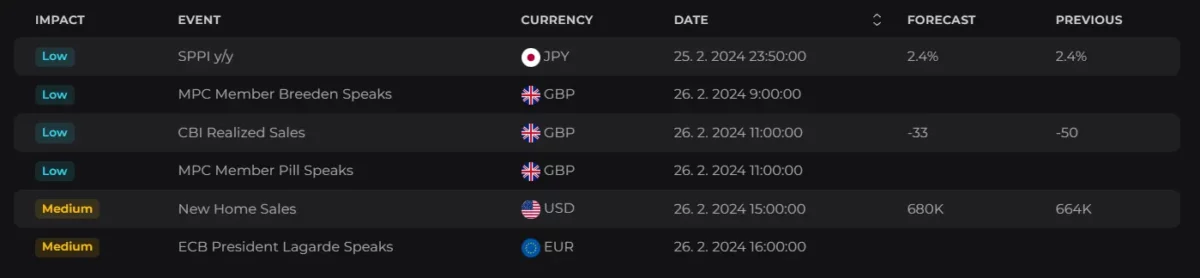

Monday, February 26th, 2024

The week kicks off on Monday afternoon with ECB President Ms. Lagarde participating in a plenary debate on the ECB Annual Report 2022 in France at 3:00 pm. However, this speech is not expected to impact market dynamics.

Simultaneously, the U.S. Census Bureau will be releasing the latest figures on New Home Sales in the country.

Toward the end of the day, at 11:30 pm, Japan’s Ministry of Internal Affairs & Communications will unveil the latest inflation trends. In December 2023, Japan’s annual inflation rate decreased to 2.6% from 2.8% the previous month, marking the lowest rate since July 2022. The core inflation rate also dropped to 2.3%, the lowest in 18 months, from November’s 2.5%, aligning with forecasts but remaining above the Bank of Japan’s target for the 21st consecutive month. On a monthly basis, consumer prices rose slightly by 0.1% in December, after no change in November.

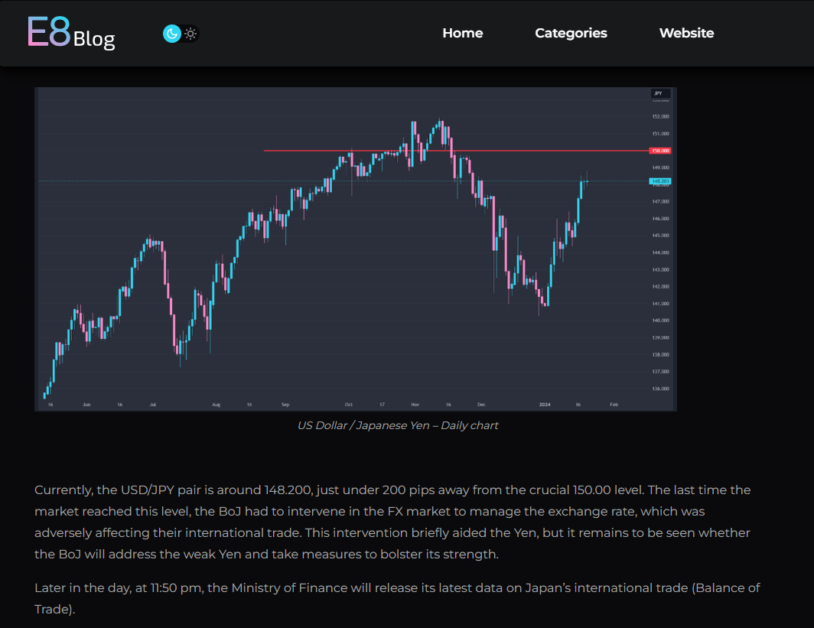

In the last week of January 2024 Market Overview, there was speculation about whether the Bank of Japan would act to counteract the yen’s weakening, or if we would see the 150.00 level reached again. Currently, as shown in the USD/JPY chart below, we are trading above this crucial level, approaching the 30-year high of 152.000 recorded on November 13, 2023. Should the pair surpass the next milestone, the historical peak of 160.000 from April 1990 is within reach. While the Federal Reserve maintains a hawkish stance due to tight labor market conditions, the Bank of Japan has limited tools to strengthen the yen besides direct intervention. Without action from the bank, there appears to be little to prevent further increases in the pair.

Speeches:

- 09:00 am – BoE Sarah Breeden

- 11:00 am – BoE Huw Pill

- 11:40 pm – FED Jeffrey R. Schmid

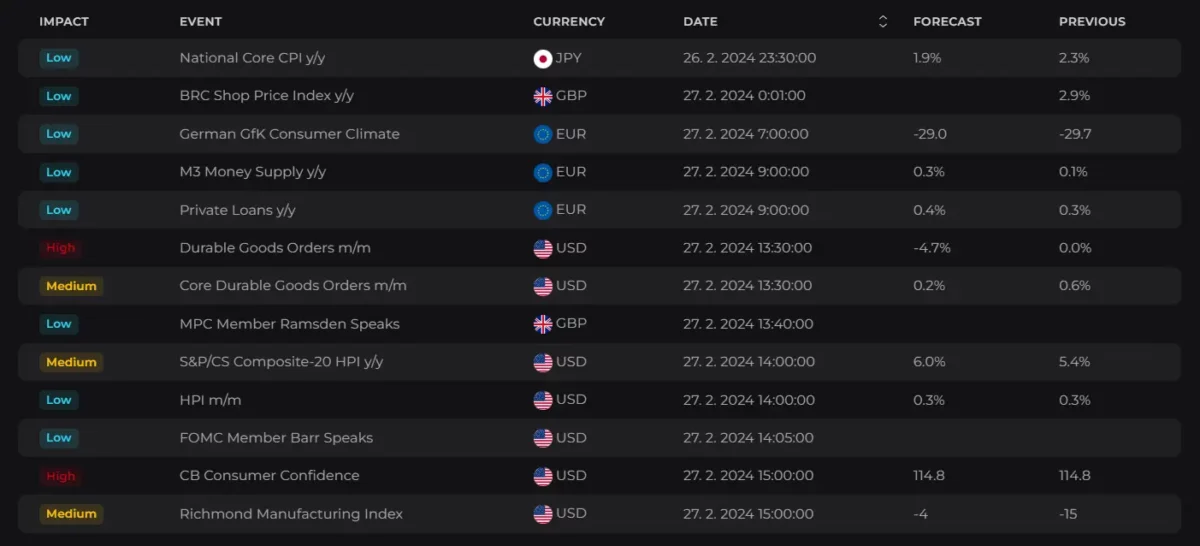

Tuesday, February 27th, 2024

Tuesday begins in Germany with the GfK Consumer Confidence Index, which unexpectedly dropped to -29.7 from a revised -25.4 in January. This latest figure significantly undershot the market predictions of -24.5, marking the lowest level in 11 months due to falling income expectations. The GfK Consumer Climate Indicator, derived from a survey of over 2000 individuals aged 14 and above, measures components such as income expectations, propensity to buy, and savings habits. Scores range from -100 to +100, with 0 indicating the long-term average. Currently, the consensus stands at -29 points, indicating a minor improvement but still reflecting a challenging outlook for the German consumer sector.

No other significant data are expected until midday. At 1:30 pm, attention shifts to the US, with a series of releases beginning with Durable Goods Orders, followed by the House Price Index and CB Consumer Confidence.

The rest of the day is anticipated to proceed without any major releases likely to alter market dynamics significantly.

Speeches:

- 01:40 pm – BoE Dave Ramsden

- 02:05 pm – FED Michael Barr

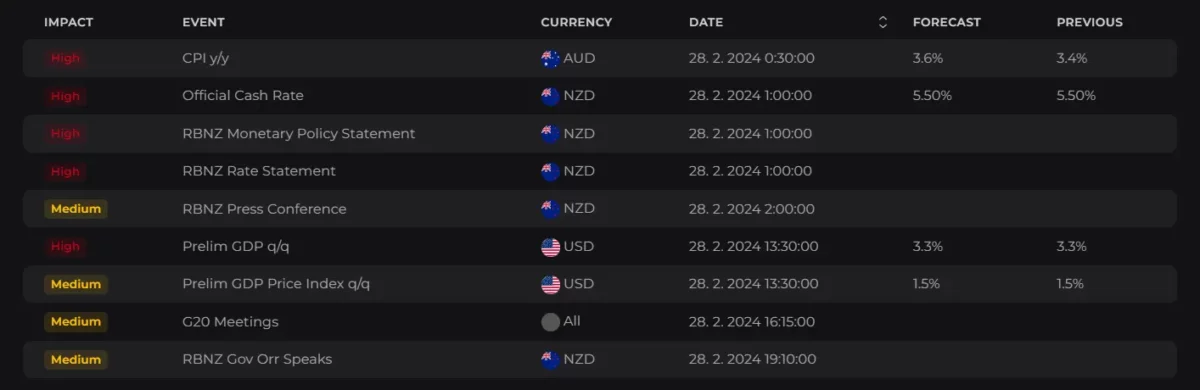

Wednesday, February 28th, 2024

The day kicks off in Australia with the Monthly CPI Indicator. The Consumer Price Index (CPI) in Australia rose by 3.4% in the year ending December 2023, a decrease from 4.3% in November and below the expected 3.7%. This marks the third consecutive month of declining annual inflation, reaching its lowest point since November 2021, primarily due to reduced increases in food prices and housing costs, including electricity, gas, and other household fuels. Despite inflation remaining above the RBA’s target range of 2-3%, the bank is not anticipated to announce a hawkish policy statement at its next meeting on March 19th.

Shortly after the Australian CPI release, the RBNZ (Reserve Bank of New Zealand) will decide on its monetary policy, including the benchmark interest rate. The expectation is that the bank will maintain the rate at 5.5%, as New Zealand’s annual inflation rate decreased to 4.7% in the quarter ending December 2023, down from 5.6% in the previous quarter. The rate decision will be closely watched, particularly during the press conference an hour before, as it could reveal the bank’s expectations for the upcoming months. Often, it’s the press conferences or speeches by bank officials that drive market momentum by outlining potential changes in response to recent economic data.

At 9:00 am, Switzerland will release its Economic Sentiment Index, followed by the Eurozone at 10:00 am.

The Swiss Economic Sentiment Index improved by 4.2 points to -19.5 in January 2024, reaching its highest level in nearly a year and signaling a reduction in pessimism about the Swiss economy, according to UBS. The consensus for this week’s reading is at -17, indicating potential further positive developments for Switzerland.

Conversely, the Euro Area’s economic sentiment indicator dropped slightly to 96.2 in January 2024, matching market expectations and slightly down from December’s seven-month high of 96.3. This suggests a gradual improvement in the European economic situation following a challenging end to 2023.

Another significant event will occur at 1:30 pm when the U.S. Bureau of Economic Analysis releases the latest GDP Growth Rate estimates. The U.S. economy is reported to have expanded by an annualized 3.3% in Q4 2023, surpassing the 2% growth forecast and following a 4.9% growth rate in Q3. For the full year 2023, the U.S. economy grew by 2.5%, compared to 1.9% in 2022, slightly below the Fed’s estimate of 2.6%. These figures, coupled with a tight labor market, support the Fed’s strategy of maintaining higher interest rates, which in turn strengthens the dollar against other currencies.

Additional data from Japan, including Industrial Production and Retail Sales, will be released just before midnight.

Speeches:

- 02:00 pm – ECB Elizabeth McCaul

- 03:30 pm – BoE Catherine L Mann

- 05:00 pm – FED Raphael Bostic

- 05:15 pm – FED Susan Collins

- 05:45 pm – FED John Williams

Thursday, February 29th, 2024

Thursday is set to be another packed day, beginning once again in Australia. New Zealand will kick things off by disclosing its Business Confidence, followed by Australia’s Housing Credit and, more significantly, Retail Sales at 12:30 am. Japan will then report Housing Stats at 5:00 am.

Transitioning to Europe, Germany will announce its Retail Sales figures. Additionally, the first, second, and fourth largest European economies will disclose their estimated Inflation Rates:

- 7:45 am: France

- 8:00 am: Spain

- 1:00 pm: Germany

These figures are critical as the European Central Bank’s (ECB) rate-cut decisions loom, with inflation being a key determinant. A drop in CPI across European countries could fuel speculations that the ECB might opt for a rate cut as early as the second quarter of 2024. Therefore, monitoring the upcoming labor market and economic growth data is vital for a clearer insight into the ECB’s forthcoming actions. Germany will also provide labor market data at 8:55 am.

Simultaneously, at 8:00 am, the Swiss State Secretariat for Economic Affairs and the Swiss Economic Institute will unveil the last quarter’s GDP Growth Rate for 2023 and the KOF Leading Indicators. The KOF Economic Barometer, a measure of business optimism and economic performance expectations, utilizes 219 indicator variables for its computation, primarily excluding the construction and banking sectors and representing over 90% of the Swiss GDP.

By 9:30 am, the Bank of England (BoE) will release data on Consumer Credit, Mortgage Approvals, and Lending.

In the afternoon, Canada will report its GDP Growth Rate at 1:30 pm. The Canadian economy experienced a contraction of 1.1% in annualized terms in the third quarter of 2023, marking its first shrinkage since the second quarter of 2021. This was a significant deviation from the expected slight expansion. However, the current consensus for the last quarter is more optimistic, with a forecasted expansion of 0.8%.

Simultaneously, the United States will commence its data release:

- 1:30 pm Core PCE Prices Index

- 1:30 pm Personal Income and Spending

- 1:30 pm Initial Jobless Claims

- 3:00 pm Pending Homes Sales

The number of US unemployment benefit claims dropped by 12,000 to 201,000 for the week ending February 17th, significantly below the anticipated 218,000, reaching its lowest since a 16-month low recorded five weeks prior. Furthermore, continuing claims decreased by 27,000 to 1,862,000 in the preceding period, below the expected 1,885,000, indicating an easier time for unemployed individuals to find jobs. This data supports the strong jobs report from January, highlighting the tightness in the US labor market and potentially giving the Federal Reserve more reason to maintain higher interest rates if inflation persists. The consensus for this week’s figures is at 210K, which, if met, indicates a modest increase. However, given that last week’s expectations were off, we might witness continued tightening in the labor market.

Speeches:

- 03:50 pm – FED Raphael Bostic

- 04:00 pm – FED Austan Goolsbee

- 06:15 pm – FED Loretta Mester

- 11:30 pm – BoJ Takata Hajime

Friday, February 1st, 2024

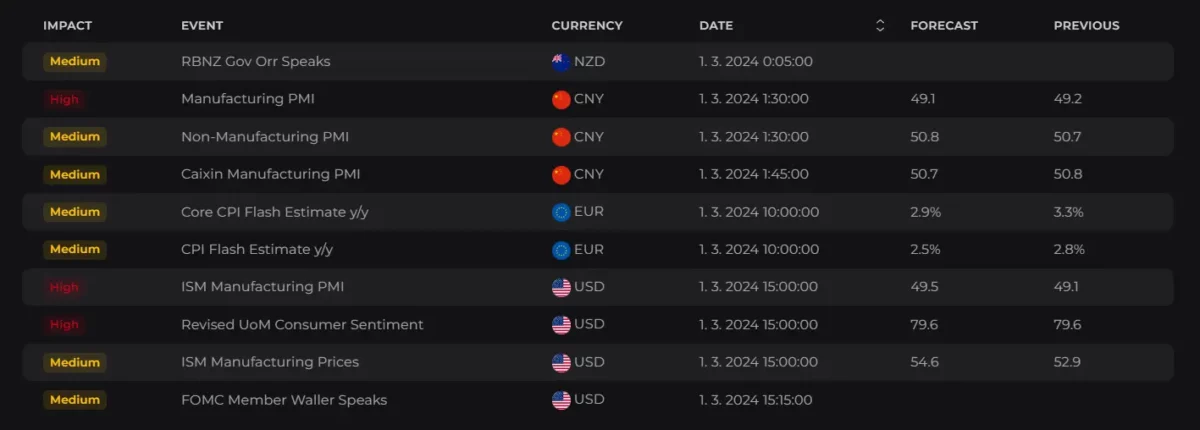

Friday begins with key updates from China. At 1:30 am, the National Bureau of Statistics of China will unveil the Manufacturing PMI. The previous report in January 2024 showed a reading of 49.2, aligning with market predictions and slightly up from December’s six-month low of 49.0. However, this marked the fourth consecutive month of contraction in factory activity, as challenges such as deflation pressure, weak demand, and ongoing issues in the property sector hampered Beijing’s efforts to revive the economy.

Just 15 minutes later, the Caixin Manufacturing PMI will be disclosed, which surprisingly stood at 50.8 in January 2024. This figure remained consistent with December’s reading and exceeded market expectations of 50.6. This indicated the third consecutive month of expansion in factory activity, presenting a contrast to the official data, which suggested prolonged weakness even before the Lunar New Year celebrations.

At 5:00 am, Japan’s Cabinet Office will report the latest Consumer Confidence Index, which has been on an upward trajectory for four consecutive months, often surpassing market expectations and indicating an improvement in household sentiment across all components.

Retail Sales figures for Switzerland will be released at 7:30 am, followed by the country’s Manufacturing PMI at 8:30 am.

Significant data from Europe will follow at 10:00 am when Eurostat is scheduled to publish the Flash Inflation Rate for the Eurozone. The inflation rate in the Euro Area was last recorded at 2.8% in January 2024, remaining relatively stable from December’s 2.9% but still above the European Central Bank’s target of 2.0%. The current consensus for the Flash CPI is now at 2.5%, which could further support the likelihood of early rate cuts by the ECB.

The week concludes with the release of the ISM Manufacturing PMI for the US at 3:00 pm.

Speeches:

- 01:10 am – FED John Williams

- 02:00 pm – BoE Huw Pill

- 03:15 pm – FED Christopher Waller

- 05:15 pm – FED Raphael Bostic

- 06:30 pm – FED Mary C. Daly

- 08:30 pm – FED Adriana Kugler

E8X Dashboard

If you’re new to our Economic Calendar, explore our detailed guide to learn more!

The Trader’s Toolbox: Mastering the Economic Calendar

Stay ahead of key economic events and data releases with our E8X Dashboard. It’s all there under the Economic Calendar tab, offering a user-friendly interface for your convenience.

Article topics

Trade with E8 Markets

Start our evaluation and get opportunity to start earning.Suggested Articles:

Disclaimer

The information provided on this website is for informational purposes only and should not be construed as investment advice. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. We do not endorse or promote any specific investments, and any decisions you make are at your own risk. This website and its content are not responsible for any financial losses or gains you may experience.

Please consult with a legal professional to ensure this disclaimer complies with any applicable laws and regulations in your jurisdiction.